This is what every democratic government should do to fix their economies. (Undemocratic governments, too.)

Monetized deficits to provide tax relief can stabilize our economies. It's the best, most productive way out of our current crisis.

I’m writing this because I genuinely think this is a way for countries - democratic and not - to stabilize their economies worldwide.

A couple of days ago I was doomscrolling through social media when a post popped up that Canadian fixed mortgage rates had gone up this week, because the market is starting to price in the impacts of Donald Trump’s economic promises.

Intrigued, I searched and found that U.S. mortgage rates had gone up (despite a Federal Reserve drop in interest rates). The explanation was:

“Treasury yields surged on Wednesday as market participants strapped in for a Trump presidency that's expected to boost inflation and interest rates.

Experts expect rising yields to lift mortgage rates in the coming weeks, though rates are expected to continue to trend downward over the long term.

Economists say Trump's tax and tariff policies could stoke inflation and deter the Fed from cutting interest rates as much as previously expected.”

Now, I fully expected that Trump’s policy proposals would have a negative economic impact. Every other political, moral and value objection aside, there is also such a thing as disagreeing with people about the way something works, and how to fix it.

I have a different understanding of the mechanics of the economy. Based on evidence and the evidence-based writings and observations of historians and economists, I think the economy actually works differently than people assume.

If you’ve ever had the misfortune of trying to start an old engine, there may be number of ways you can foul it up. You can end up having an argument with someone about why they’re not fixing something properly, because you are disagreeing about the way it actually works. We don’t agree that when you push that button or pull that lever, that it’s not going to do what you think it will.

And that is very much the problem with Trump’s plan, and his economics, which it is that it will have the opposite effect of what is intended.

Growing Mortgage Defaults a Key Warning Sign

There’s a saying that when a structure collapses, it does so at its weakest point.

In an economy, the weakest point is the individual borrower who has debt on a non-productive asset: someone who has a mortgage on their home.

One of the major underlying signs of the economic insecurity that drove Trump’s victory was that mortgage delinquencies have been growing steadily for over a year.

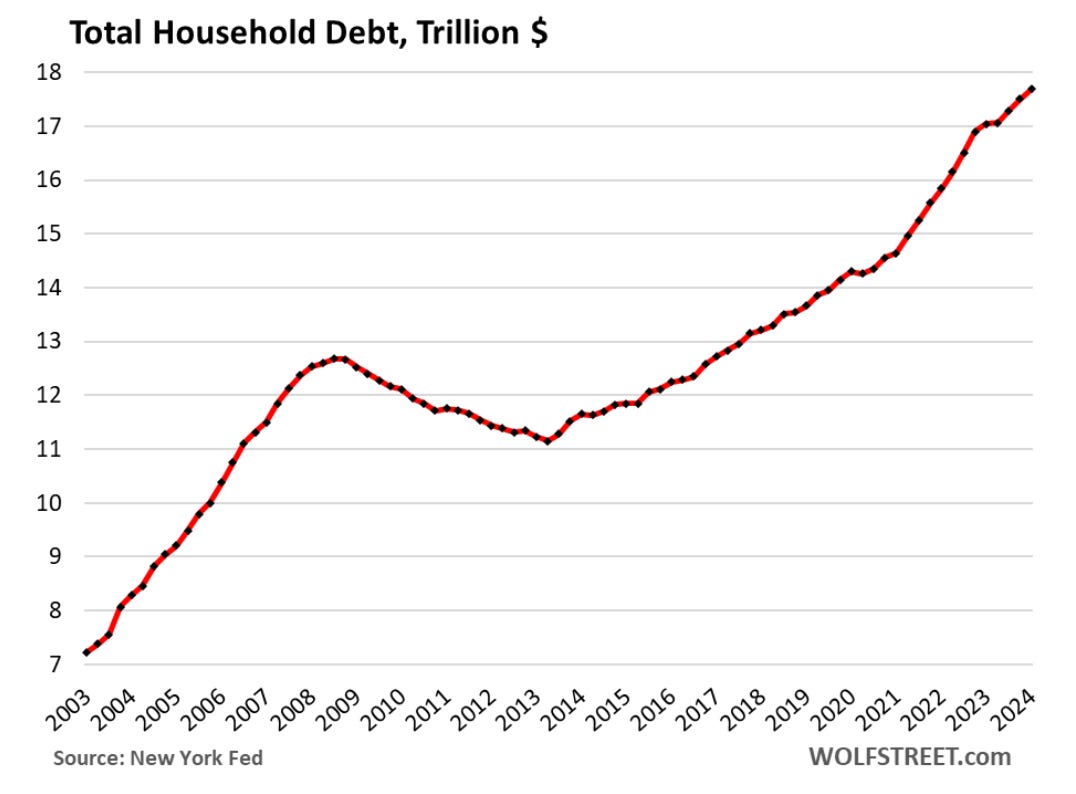

In the U.S. total household debt was $17.7- trillion. In Canada, it was close to $3-trillion. Both are reflections of the massive housing and asset bubbles in these countries. The thing is, every borrower requires a lender - and there are a lot more borrowers than lenders.

So, all that household debt is actually the assets of a small percentage of the population.

It’s not complicated: The more you go into debt, the richer your lender gets, and the poorer you get. And every time there’s a crisis, the solution has been to make it easier for you to go deeper into debt. Lower interest rates for bigger mortgages, and credit cards instead of a raise.

The economists and economic historians and other observers of markets and market crashes that I have followed emphasize the critical role of private, household debt.

There’s no question that collapsing mortgages were the cause of the global financial crisis. But the blame is put on the borrowers, not on the people who cooked up a failed scheme.

It is incredibly hard for many people to understand how crushing the weight of debt is for people, and the worry associated with it. Most people’s worth is tied up in their home. If they lose that, they lose everything, and you can lose it because circumstances out of your control change. A pandemic. A recession. Inflation. Interest rate hikes. Imagine for a moment the fear and loss that you would experience if you faced losing everything you worked for. The assumption is that people who take out debt are always to blame for their own misfortune, when the core economic ideology since the 1970s has been that consumers can drive a recovery by taking on more debt.

We are not in a “hot” economy: we are in an irrational and manic economy

One of the reasons Trump was elected was that there really is growing income and economic insecurity. An important sign of this is mortgage delinquencies, which are growing in Canada and the U.S. In September, MarketWatch reported that U.S. mortage delinquencies had “ticked up” for the fourth month in a row.

On November 4, it was reported that

“New insights from Bank of America show that people across income brackets, whether earning less than $50,000 or over $150,000, continue to report living paycheck to paycheck. Nearly half of those surveyed agree with the sentiment of tight budgets, as daily essentials like gas, food and health care "swallow up" their earnings.… With interest rates high, financing costs for essentials like car loans or home improvements are pushing monthly budgets to the brink.”

This is not a “hot” economy. This economy showing all the signs of “Pre-crash mania” which we is manifesting it a stock market that is soaring, along with all sorts of other desperation, panic, and get-rich quick schemes.

I will say briefly, that I recognize these things, because I’ve lived through several of them. At university in the 1980s, there was a boom - and a spread of pyramid schemes, just before a major economic crash. In the 90s, there was a boom with the .com bubble but also with Beanie Babies or baseball and trading cards. More recently, we have had crypto, NFTs and meme stocks. They are all symptoms of an irrational market.

The problem, as Keynes said, is that the market can stay irrational a lot longer than you can remain solvent.

The Price of Uncertainty

It’s important to be clear about interest rates and inflation, because there is another very important way to interpret them.

The current interpretation of inflation and interest rates is that they are related to the quantity of money - the idea that if you add money to the system, it “dilutes” the overall pool of money. This is intuitive, but it depends on a system where everything is known. This is actually one of the premises of “rational choice” theory of economics, which asserts total certainty.

I would like to propose another explanation, which is that interest and inflation are both a price on uncertainty, and uncertainty is missing information.

For markets, this may translate into emotions ranging from anxiety to fear to panic. And each of these is related to the level of uncertainty - which is about missing information.

Take the individual, personal example of getting a loan. The terms of the kind of loan you can get is directly related to how certain the lender is that you will pay them back. The less they are sure they will be paid back, the higher your interest rates will be. Inflation tends to rise in times of crisis and uncertainty. This is true from supply chain disruptions to panic buying and price-gouging in emergencies and natural disasters.

Missing information and uncertainty raises volatility. And it has to be said, that when it comes to gains for investors, this also tends to drive inequality, as well as crisis. The largest fortunes are lost and made, not gradually over time, but on the days with the greatest volatility. By their very nature, low-risk investments pay off for many investors. The investment pays off and is spread over more winners and fewer losers. High-risk investment, means that most investors will lose and that a few will win big - the losses of the many go into the pot of the winner.

How to Escape The Current Trap

Now, there is an alternative to all this madness, which every country could take, and that would likely work.

So here’s the simplest way to explain how a central bank could act in an emergency to provide economic relief, right now.

Let’s say you have the complete Canadian federal budget ready to go. You know how much revenue from income tax. It’s been $175- billion in recent years.

Due to an economic emergency, you want to help citizens, you could say “this year, and this year only, we will cut personal income taxes by 25%.” Everyone still files their taxes - but at the end of what you’ve calculated, you’ll pay 25% less (or you’ll get a 25% rebate).

For the government, that means $43.75-billion less in revenue. To keep the budget in balance, normally what you would to would be to sell bonds and go to private investors, or cut back and fire people or reduce government payments.

However, if you do this, it undermines the benefit of the tax cut. If you are running a deficit and borrowing, you will have to pay back the benefit of the tax cut with interest. If you are going to cut $43.75-billion from government spending, you’re just robbing from Peter to pay Paul. You’re making one group better off at the expense of another.

Instead, you create an agreement that this year the central bank will create that exact sum in new money - $43.75-billion - and give it to government to replace the otherwise lost revenue.

This is what is known as a “monetized deficit”, although it could also be considered “helicopter money.” It is effectively an injection of cash into the economy, and it is a very specific amount, for a very specific purpose. Every Canadian knows exactly where the money is being used. Every taxpayer gets relief. And government can also continue to make needed investment without taking on more debt.

That is a “monetized deficit”. As Biagio Bossone explains:

“The monetization of fiscal deficits – that is, budget expenses in excess of revenues – involves the financing of such extra expenses with money, instead of debt to be repaid at some future dates. It is a form of "non-debt financing". Thus, monetization of fiscal deficits can occur only through one of two modalities:

First, the sovereign (government) prints its own money and finances its expenses. In practice, the same happens as the fiscal deficit is financed with newly created money issued by the central bank and transferred to the state treasury without future repayment obligations: the money issued by the central bank is either credited to the account of treasury or treasury is allowed an overdraft facility. Debt would obviously originate if treasury were to borrow the money from the central bank; yet, this would not constitute true monetization of the deficits, but simply a temporary support to treasury cash needs.

According to an alternative (and more convoluted) modality, fiscal deficits are monetized as the government issues bonds in the primary market and the central bank purchases an equivalent amount of government bonds from the secondary market. Importantly, however, and this is commonly the forgotten part, for this modality to replicate the same effects of the first, the central bank must commit to the following actions: i) hold the purchased bonds in perpetuity, ii) roll over all the purchased bonds that reach maturity, and iii) return to government the interests earned on the purchased bonds (Turner, 2013).”

This kind of financing is actually one of the ultimate ways that a democratic government can do to assert and maintain its sovereignty - that it’s possible, in emergencies, to fund the government this way without taxes. In fact, it is the exclusive right of government and public institutions, not private ones. It’s how the U.S. paid for 15% of the Second World War effort.

If anyone is concerned with the idea that this sum of money will be incredibly economically disruptive or inflationary ask yourself this - if you got back 25% of your taxes back, would you use it to drive up prices? Of course not. We need to reject the bizarro-world explanation of the economy that citizens and customers spending a few thousand dollars each is what drive prices up.

If you got 25% of your income taxes back, you know that you could use it, but there’s no way you’re going to be driving up any prices with it.

To be fair, there are people who pay no taxes who could also benefit - seniors, people with disabilities, veterans. So could commit to reducing everyone’s personal income taxes by 25% (or another amount) and also commit to a minimum benefit.

William Buiter wrote a paper analyzing the impact of a helicopter money in the rather provocatively titled “The simple analytics of helicopter money: Why it works - always” in which he wrote

The author provides a rigorous analysis of Milton Friedman's parable of the "helicopter" drop of money a permanent/irreversible increase in the nominal stock of fiat base money rate which respects the intertemporal budget constraint of the consolidated Central Bank and Treasury - the State. Examples are a temporary fiscal stimulus funded permanently through an increase in the stock of base money and permanent QE - an irreversible, monetized open market purchase by the Central Bank of non-monetary sovereign - debt. Three conditions must be satisfied for helicopter money always to boost aggregate demand. First, there must be benefits from holding fiat base money other than its pecuniary rate of return. Second, fiat base money is irredeemable - viewed as an asset by the holder but not as a liability by the issuer. Third, the price of money is positive. Given these three conditions, there always exists - even in a permanent liquidity trap - a combined monetary and fiscal policy action that boosts private demand - in principle without limit. Deflation, "lowflation" and secular stagnation are therefore unnecessary. They are policy choices.

Now, for people who want to say that this is not reasonable, or that it will be disruptive, or cause inflation, or that international markets will object, I have to make a couple of points.

First, especially since 2008 and the Global Financial Crisis, central banks have created trillions of dollars in order to prop up the reserves of failing banks.

This also happened during the pandemic. In Canada, in just two years, the Bank of Canada printed $300-billion for the financial sector.

the Bank of Canada, under several large-scale asset purchase programs to increase liquidity in core funding markets. From March 2020 to March 2021, investments held by the Bank increased by over $300 billion, largely reflecting market purchases of Government of Canada bonds. This growth is offset by a corresponding increase in the Bank's liabilities for bank notes in circulation and deposits.

Since the Global Financial Crisis, the amount of large-scale asset purchases has been in trillions. The same policy happened in Canada, the UK, the EU.

The global pandemic was declared on March 12, 2020. In March 2020, the commitment from Federal Reserve Chair Jerome Powell was that there would be no limit to QE:

“Saying “aggressive action” was needed to soften the blow to the economy from the coronavirus pandemic, the Federal Reserve on Monday announced it would purchase an unlimited amount of Treasurys and securities tied to residential and commercial real estate to ward off a credit crunch. [Emphasis mine].

When asked how it was done, Jerome Powell answered, with a touch of a button.

I have to make a point here about words like “infinite QE” or “unlimited QE.”

There are right-wing economists and ideologues - Austrian economists, libertarians, fiscal conservatives who catastrophize the power of the federal reserve to create money.

They are missing the central point and value of the central reserve. It is not about creating unlimited amounts of money, or infinite amounts of money.

The money creating power of central banks is about the absolute certainty that money can be created. Always. It’s not about the unlimited creation. It’s about being sure that money can always be created. That is actually a key role of government in the economy.

If I am correct in thinking that inflation and interest rates are both due to growing uncertainty and missing infomation, then helicopter money through monetized deficits would stabilize the economy by reducing uncertainty.

This is something that could be done in governments all over the world. Similar financing can also be used to support public investments in infrastructure and jobs.

The reason these measures are opposed by right-wing economists and propagandists is not because it will be harmful for the economy, but because the private sector is demanding protection and even further extension of their private monopolies and oligopolies, which include finance, tech and oil.

Canada could do this. The UK can do this. The US can do this. There are challenges for the EU, but they could, in principle, do this as well. The obstacle is ideology, which is to say, mistaken beliefs about the way the economy must work, and not practical.

We could have a multi-country agreement where every country in the world agrees to do this. It could be done for one year or over a period of five years.

Dealing with objections

Objection 1 - German Hyperinflation

While people will often raise the bogeyman of German Hyperinflation, as I have written, while that is one of the most famous examples of hyperinflation, our history of it is completely wrong.

German hyperinflation was not caused by government printing money. It was caused by private banks creating money. A rule had been created that effectively allowed private banks to create unbacked IOU’s that could be cashed in for “real money” on demand at the central bank. When that practice was ended and a new currency released issued, the hyperinflation stopped immediately.

Objection 2 - The International Financial Markets

One of the objections here is “what about international financial markets”? or the idea that Canada will be punished for doing this, or that no one will want to buy Government of Canada (or provincial) bonds.

At this point, the question has to be asked whether the tail is wagging the dog here.

Since 2008, international financial institutions have required, and received more than $20-trillion in quantitative easing from central banks, so that these institutions would not go bankrupt.

This is a genuine question to anyone who can answer it - how we can be at their mercy, when they were just bailed out with $20-trillion in public money?

Central Bank Independence

This can all be accomplished with the voluntary cooperation of central banks. It is not a question of politicians telling central banks what to do, but of central banks realizing that this is a viable policy and cooperating with governments to do it.

Why it will work

We need to understand something very important about the market - which that uncertainty and volatility is bad for the vast majority of investors. Volatility contributes to greater losses for small investors and debtors.

The reality of our economy is that if this were all one big casino, people are getting angry because the same people keep winning, because for most people, their gamble didn’t pay off.

That’s the essence of the market, right there. Everyone plays, and in finance, it’s a zero-sum game. For someone to make a dollar, someone else has to lose one.

That’s different than the “real economy,” where there is is no loser. One side, gets money, the other gets something for the money. That’s industrial capitalism. It’s different than financial capitalism, which is what we’ve had since about 1978. That’s when incomes started diverging: centre and centre left governments around the world

The reason that the 1970s ideas of neoclassical economics and neoliberal ideas were brought in was for a very specific academic reason, which is that the supposedly Keynesian economic models they followed had failed to predict stagflation. However, Miltion Friedman had, so his theories became the official dogma of central banks and various economic agreements.

The bitter irony is that as soon as the centre and centre-left 1970s governments of Jimmy Carter, Pierre Trudeau and Harold Wilson implemented these neoliberal ideas, incomes started to diverge, as they have continued to do ever since.

What people fail to realize that what is holding them back the most - and is one of their greatest costs, is not taxes or groceries or energy, it’s the debt they have to pay every month.

Injecting a specific, controlled amount of cash - nor credit - into the economy in this fashion has the effect of de-risking the economy.

You could double the amount, or make it for two years. But for now once governments would be doing something where everyone knows they all got a fair treatment.

Monetized deficits like this could be used to invest in putting people to work or in infrastructure that creates new value.

Large monetized deficits shouldn’t be common. They’re for emergencies. They can set an economy right then they can go back to being low or non existent. Only federal governments with monetary sovereignty can do this. Lower levels of government should aim for balanced budgets.

This is something that literally every country in the world with its own currency should be able to do. It would be best that it’s simply agreed that this is what each country will do and keep it simple. A certain percentage of income tax for a fixed period in every country. Funds could also be used to re-industrialize through the provision of access to capital for entrepreneurs.

This is the best possible way for developed nations and governments to deal with the economic and housing crises. Inflation, interest rates and austerity all create more uncertainty.

In Canada, especially, the Bank of Canada’s mandate is broad:

“WHEREAS it is desirable to establish a central bank in Canada to regulate credit and currency in the best interests of the economic life of the nation, to control and protect the external value of the national monetary unit and to mitigate by its influence fluctuations in the general level of production, trade, prices and employment, so far as may be possible within the scope of monetary action, and generally to promote the economic and financial welfare of Canada.”

We are in a new economic age, because the old economic age is not serving the needs of the people, and the people are letting us know.

-30-

Uncertainly DOES play a role in interest rates as well as bond prices. I agree completely with the analysis but I would tweak the Rx just a bit.

A one-time tax rebate would be a regressive way to distribute the money back to taxpayers. And if debt relief is the goal, I am not sure a one time rebate would do much for that. When I first started working I eavesdropped on a conversation the head of my department was having with a colleague saying that when they were earning a good income it was easy to get credit anywhere but when you really needed it was when you were first starting out. “YES” I said to myself internally!

Older/wealthier individuals may not have debt that is a problem for them to manage but younger and less well off individuals certainly need the help. Plus there are people who cannot take on debt of virtually any kind because their incomes are so low plus no collateral.

So… I would take 25% of income tax receipts (including corporate taxation) and rebate that as a monthly payment that is subject to tax after the first 15000 or so. This would be much like the OAS now, and would be available to anyone filing a tax return.

Coupled with targeted spending on public housing projects and infrastructure hardening/upgrading this would be a winning strategy anywhere.

This makes eminent sense on many levels.