Central Bank Policies are Killing Democracy and Ruining the Economy. We Need Change Now.

Bullshit Billionaires, Market Bubbles, Bankrupting Business and the Middle & Working Class. Central Banks wholesale, economy-wide manipulations of market and debt have destroyed real value.

While everyone blames politicians, the real culprits are the reality-denying policies of central banks. They create bubbles & bullshit billionaires while bailing out banks and bankrupting everyone else.

While some economic indicators in Canada are ripping higher, the struggles Canadians are facing are undeniable, and the current policies of the Bank of Canada massively adding stress to Canadian businesses and families alike, in the name of fighting inflation.

The Bank of Canada is punishing Canadian borrowers who are being crushed by inflation that’s being driven by international factors like energy and supply chains, as well as by an asset bubble and a domestic debt crisis here in Canada. When that happens, government revenues dry up as well. A double-whammy, and a guarantee of austerity under fiscal conservatism, driven by a central banks that have printed hundreds of billions of dollars to bail out investors, while asking everyone else to tighten their belt.

That explains articles like this - https://apple.news/A6bcCqJqSR-iOAp6yXoBkBQ

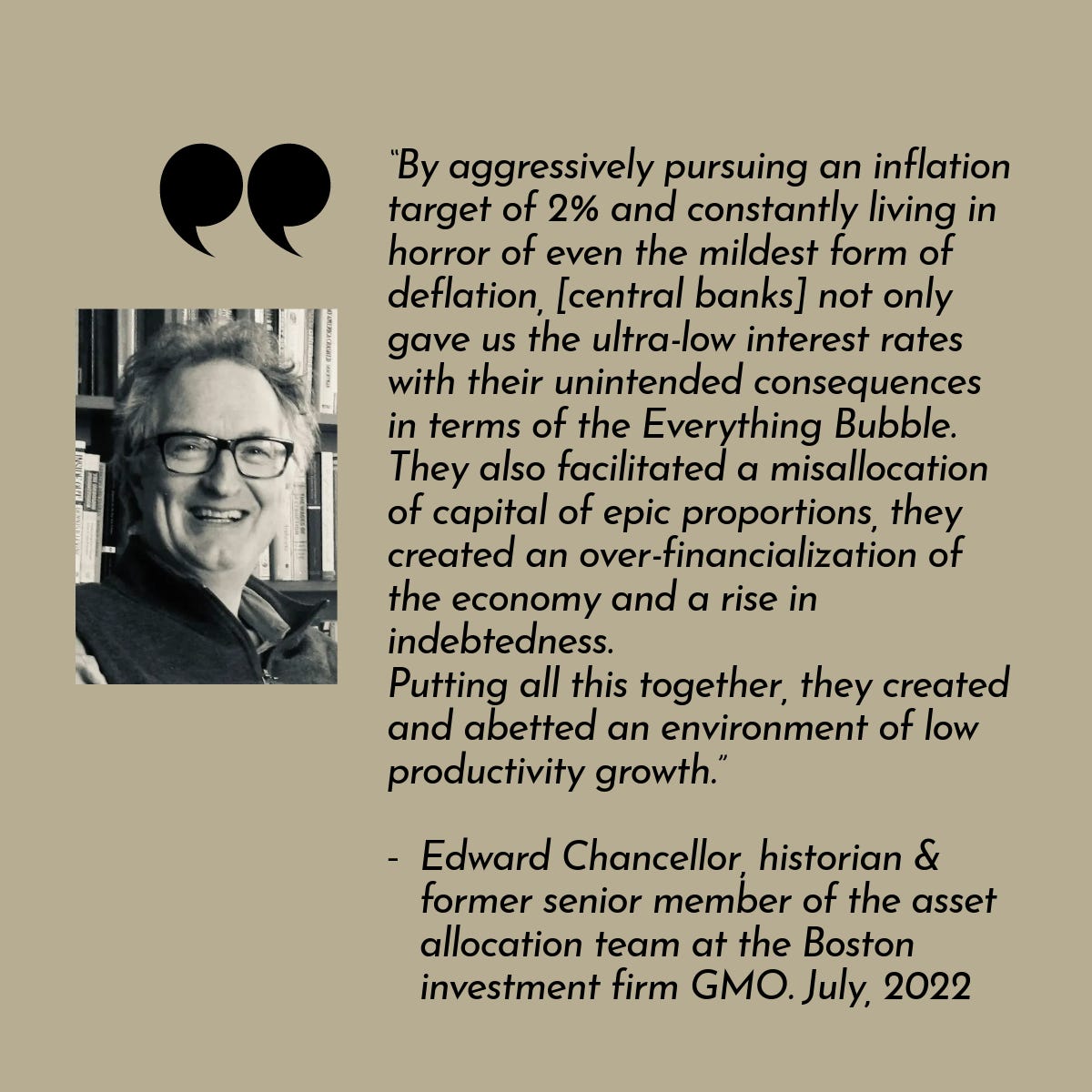

In July 2022, Edward Chancellor warned

“It will turn out to be largely impossible to normalize interest rates without collapsing the economy,”

– not because of the actions of elected governments and officials, but because of two decades of monetary policy pursued by the Bank of Canada and other central banks, which are independent and are supposed to be free from political influence.

https://themarket.ch/interview/edward-chancellor-central-banks-delayed-the-day-of-reckoning-ld.7051

Says Chancellor

“By aggressively pursuing an inflation target of 2% and constantly living in horror of even the mildest form of deflation, they not only gave us the ultra-low interest rates with their unintended consequences in terms of the Everything Bubble. They also facilitated a misallocation of capital of epic proportions, they created an over-financialization of the economy and a rise in indebtedness. Putting all this together, they created and abetted an environment of low productivity growth.”

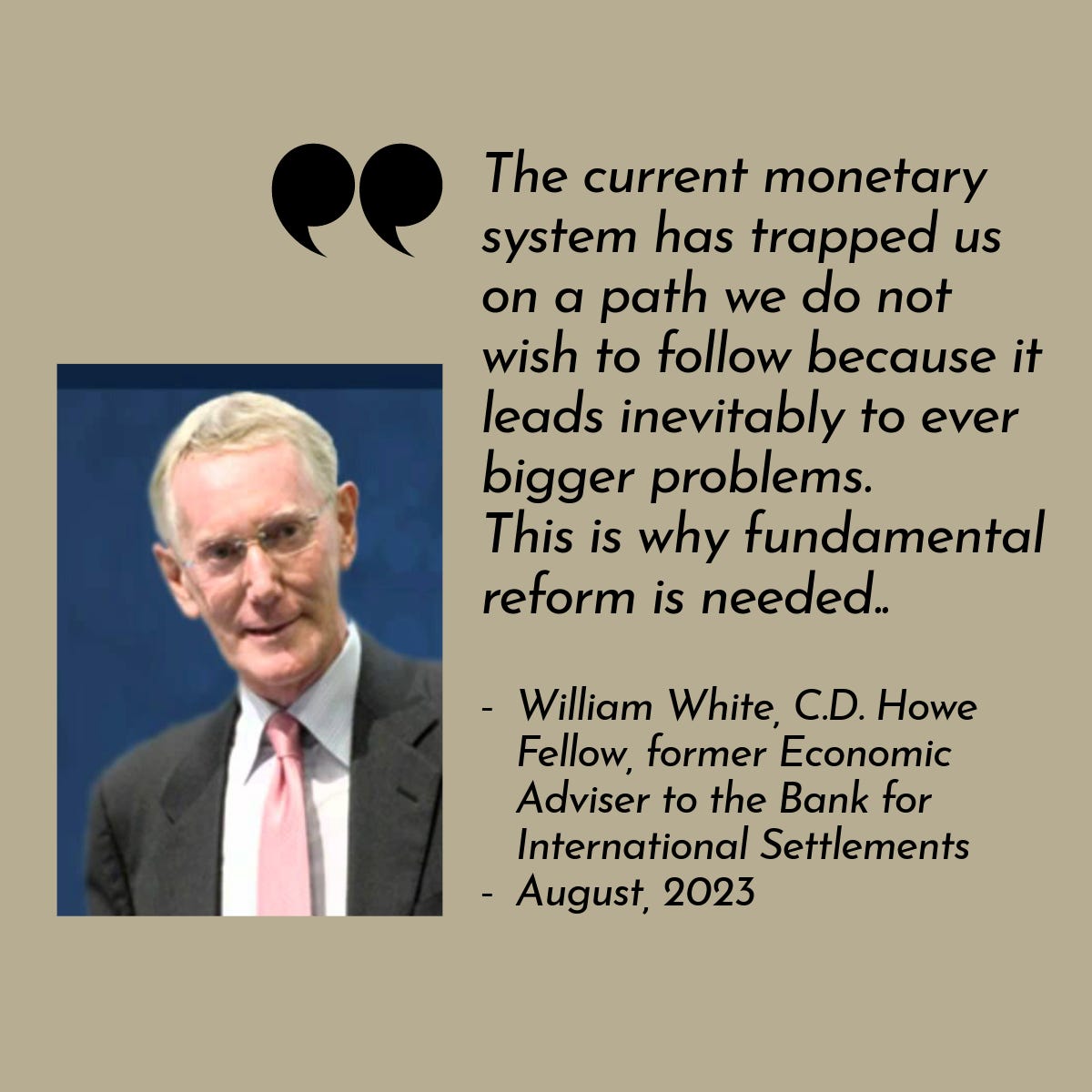

One of the first steps we need to take to deal with the issue is to immediately reform of the Bank of Canada’s monetary policy, because the current practice of cranking interest rates up and down is not only ineffective, it is actively harmful.

That is the recommendation of economist William White, from August of this year.

“[S]timulative monetary policy has had a variety of unintended and unwelcome consequences that can only worsen; credit “booms and busts”, potential financial instability, fiscal unsustainability, a progressive loss of central bank “independence”, growing inequality of wealth and opportunity and a slower growth rate of potential output. Fourth, as the threat posed by these unintended problems have cumulated over time, “exit” and the “renormalization” of policy has become ever harder to achieve.

To sum up, the current monetary system has trapped us on a path we do not wish to follow because it leads inevitably to ever bigger problems. This is why fundamental reform is needed.”

White’s Paper can be read here:

https://www.ineteconomics.org/uploads/papers/WP_210-White-Monetary-Policy.pdf

White says central banks need to focus more on the financial system and debt, and not just on inflation targets. As he points out, because of the tools central banks are using - “solving today’s problems also makes tomorrow’s problems worse”

The reason the Bank of Canada, and other central banks are doing this is because the economic models they are using are crude and terribly out of date. We can’t keep stimulating the economy by turning interest rates up and down like a volume knob, as politicians are still asking to do.

People may think of low interest rates as making debt “cheap, but so-called “easy money" drives up prices.

Low interest doesn’t mean lower cost debt. Instead of taking out the same mortgage with a lower rate, low interest rates mean a massive increase in debt across the economy:

Borrowers who already qualified can borrow even more. Corporate borrowers can use debt to finance mergers and acquisitions, resulting in the greater concentration of ownership and less competition.

At the lower end of the borrowing scale, ultra-low interest rates and “easy money” mean that debt penetrates further and more deeply into the economy.

The same payment that financed a $275,000 mortgage will now finance a $550,000 home, and people who couldn’t obtain loans at all start getting them.

For example, if a borrower can make a $2,000 monthly payment, a 30-year mortgage at 8 percent will finance about a $275,000 home.

With a mortgage rates of 4 percent, the same payment buys a $550,000 home.

The fact that the mortgage is secured against the “asset” doesn’t change that you are borrowing twice the money on the same income, and that nothing has gone into property improvements to make it worth more. You are just competing against other people’s borrowing.

As White put it, “Financial bubbles have created ever larger bubbles which threaten future growth prospects.”

One of the defining features of a bubble – or a financial mania - is that the asset being traded can’t actually be used for its intended purpose anymore. This has been true for centuries for everything from Tulip Bulbs, to Beanie Babies to Baseball Cards to Crypto. And in housing, it means that homes and condos sit empty in a housing crisis.

This is a huge problem, in multiple ways, also because it is outside the realm of democratic political decision-making.

The Bank of Canada makes its decisions completely separately from the Government of Canada. No elected official is allowed to call the shots – to keep the power from creating money through monetary policy, away from the people who spend it and fiscal policy.

So, the good news is, that if Central Banks change their policies as White recommends, we’ll at least be be able to start responding to the crisis we’re in. There are lots of policy measures we could be taking, but they won’t work unless the Bank of Canada, which sets interest rates for the whole economy, changes tack and follows White’s suggestions.

Not only does White know what he is talking about, there is arguably no one in the world who knows more about central banks than he does.

Currently a fellow at the C D Howe Institute, White was born in Kenora, Ontario in 1943. He worked “for various central banks for 39 years, most recently serving as chief economist for the central bank for all central bankers, the Bank for International Settlements (BIS)”. His time included working at the Bank of England and the Bank of Canada.

For several years, as economic advisor, White warned Alan Greenspan and other central bankers starting in 2003 - for five years - that there was a financial crisis coming.

I think you would be challenged to find anyone else in the world who has more credibility on these issues than White.

There are other economists who have been outspoken critics of the current state of macroeconomics, because they utterly failed to predict the 2008 crisis.

One of the highest profile is Paul Romer, the former Chief Economist of the World Bank, wrote a paper in 2016 called “The trouble with Macroeconomics” In it, he condemned the total failure of our mainstream, orthodox economic to predict complete disasters, like the Global Financial Crisis, when previous economic models had been tossed for much smaller failures of prediction - like getting rid of Keynes in the 1970s.

Romer wrote:

“The noncommittal relationship with the truth revealed by these methodological evasions and the “less than totally convinced ...” dismissal of fact goes so far beyond post-modern irony that it deserves its own label. I suggest "post-real."

https://paulromer.net/the-trouble-with-macro/WP-Trouble.pdf

So we have a critique by the former Chief Economist for the World Bank, saying the economic formulas used by central banks are disconnected from reality.

You also have the former advisor to the Bank of International Settlements who warned of the global financial crisis when no one else did, offering up some very sensible recommendations and reforms.

It is impossible to imagine people with better credentials, and the fact that William White predicted the single most important and disruptive economic event in a century, when virtually no one else did, only adds to the cachet.

We cannot have a repeat of what the Bank of Canada did, starting under the Harper Conservative Government in 2008-09. The entire story about strong bank regulation saving the banks was false: there was a bailout of $114-billion dollars. Comparable in size to the bailout in the U.S.

And it established the practice, which is that when banks get into trouble for lending carelessly because interest rates are so low, they don’t face consequences of their risk gone wrong, the way any other business in the free market would. Instead, the banks can take all the mortgages that are going sour because people are missing payments, and sell them to the Bank of Canada or possibly CMHC. The banks get newly created government money, the people lose their house.

The banks can sell the troubled mortgages to the central bank and get new money in return to lend out again. In 2008-09, the Bank of Canada and the Conservative Government of Stephen Harper guaranteed a $200-billion backstop. This set a pattern that kept real estate speculation- not housing, but real estate speculation - making life completely unaffordable.

This is the new model for Central Bank intervention - it is not just adjusting interest rates, it has been for central banks to print hundreds of billions of dollars - trillions worldwide which has gone to banks to lend more.

Our housing crisis is not being driven by supply or demand, it is being driven by speculation in real estate due to what is known as “easy money” – when interest rates are low, the amount of loans go up. Banks start going for quantity instead of quality.

It is this debt from easy money that is driving all the economic anxiety, from inequality and joblessness, the housing crisis, inflation, and lack of economic competitiveness. Workers can’t afford housing, so they demand raises. Companies can’t afford the overhead.

This is much more than a matter of monetary policy alone, because monetary policy underpins the entire economy.

We are talking about the stability of the Canadian economy at a time of multiple crises. Our economy is being deliberately destabilized by Putin, with higher energy prices because of the war in Ukraine, to drive inflation, and disrupt global food markets.

During and after the Great Depression, Canada and other countries ensured that we would always have the capacity to stabilize the economy in times of national or international crisis, by having the Government of Canada and the Provinces work together with the Bank of Canada and the private sector. This is not a zero-sum game where for one Canadian to win, another Canadian has to lose.

We already have the legislative tools to stabilize and reinforce Canada’s economy. The issue is ideology and policy whose models are so bad that they essentially demand human sacrifice;

It used to be recognized that inflation was, at least, a double-edged sword. In The Big Trade-Off, Arthur Okun wrote that, ‘The crusade against inflation demands the sacrifice of output and employment.’ Even more important, it should be recognized that inflation affects different constituencies and parts of the economy very differently.

Ha-Joon Chang elaborated:

a tough control on inflation is a two-edged sword for workers — it protects their existing incomes better, but it reduces their future incomes. It is only the pensioners and others (including, significantly, the financial industry) whose income derive from financial assets with fixed returns for whom lower inflation is a pure blessing.”

And that’s why William White’s recommendations for reform are so important, and why they need to be acted on with all due speed, but we are not.

Instead, central banks are blowing asset bubbles.

Yes, there are better ways of doing this.

In 2017, I presented a paper at the Cross Border International Post-Keynesian conference in Buffalo, New York detailing the ways in which Central Bank policies had made inequality worse, and had massively distorted economies by creating debt-fuelled bubbles which manage to consume worthwhile businesses as they are inflated as well as when they crash.

That is because the single-minded focus on suppressing inflation as a cure-is focused primarily on protecting one constituency, and one constituency alone - asset owners - at the expense of everyone else in the economy, whose work and investments support the real value of those assets.

It undermines the foundation of the economy by hollowing out the working and middle classes. This is absolute madness, and the fact that economists - especially central bankers - are blind to this means that they are cut off from reality.

The dangers to the economy and democracy are real.

As I have also written, financial crises and austerity lead to political polarization, brutal politics and extremism, because as honest ways of making a living through work vanish, in desperation, people turn to riskier and more speculative ventures, from shady to outright criminal.

Central bank policies are collapsing economies and killing democracy. They can find trillions of dollars when needed to bail out financial systems, while governments and the rest of the job market are crumbling.

Central Banks need new mandates, and that mandate needs to be to save the economy, and stop ruining it.

From my 2017 essay:

“The Bank of Canada was created in 1935 to help Canada deal with the Depression, whose impact on Canada was second only to the U.S. The Bank of Canada still has the power to provide interest-free loans to Canadian governments, or to inject money into the economy via monetized government deficits. The Bank of Canada did this not just during the Depression and the Second World War, but until 1975.

Unlike the European Central Bank, which is barred by the Maastricht Treaty from providing monetary assistance to governments, the obstacle to the Bank of Canada resuming this practice is ideological – it was ended at a time when concern about inflation and stagflation were growing.

In a paper examining the Bank’s role in the Canadian economy from 1935-1975, Josh Ryan-Collins found:

little empirical evidence to support the standard objection to such policies: that they will lead to uncontrollable inflation. Theoretical models of inflationary monetary financing rest upon inaccurate conceptions of the modern endogenous money creation process…during the period 1935–75… working with the government, [the Bank of Canada] engaged in significant direct or indirect monetary financing to support fiscal expansion, economic growth, and industrialization (Ryan-Collins 2015).

Ryan-Collins notes that the establishment of central banks in former British Colonies was different than the origin and purpose of central banks elsewhere – it was done to ‘establish monetary sovereignty from Great Britain,’ and not as a lender of last resort or to fund military ventures. Between 1935 and 1939, the Bank funded:

“over two-thirds of government expenditure…Nominal gross national product (GNP) expanded by 77% in contrast to the 70% contraction in the previous five years, with a sharp increase in capital investment and private expenditure… Between 20–25% of Canadian public debt was financed and held by the central bank and government from the end of World War II up to the early 1980s.

The policy of central bank financing of debt was abandoned in the mid-1970s. As Ryan-Collin mentions, this means that in the 1980s, the Canadian government was running high deficits at 20% interest, with the benefits of interest flowing out to private bondholders, instead of back to government. In 1994, the Canadian government embarked on a major austerity program when the Canadian government was facing default due to a lack of interest from the bond markets. The austerity was driven in part by not wanting to turn to the IMF, which would certainly demand draconian cuts.

On the question of inflation, Ryan-Collins’ empirical study finds no correlation between Canadian inflation and monetary injections into the economy – rather, inflation tends to be correlated to U.S. inflation. This is arguably a reflection not only of the role trade with the U.S. plays with Canada, but the role of money creation and destruction in the economy.

The trap we are in both ideological and political. While there is no new widely agreed upon paradigm, there is no shortage of theory and evidence from history that demonstrates that central banks not only can, but did play a role in reducing inequality and growing the economy, both in Canada and the U.S. Ryan-Collins’ study of Canada’s experience provides empirical and historic evidence that a central bank can intervene in the economy, supporting both government and private investment, without significant inflation. Andricopoulos has argued the case for monetized deficits to bring down private debt. In 2014, William H. Buiter argued that ‘there always exists– even in a permanent liquidity trap – a combined monetary and fiscal policy action that boosts private demand – in principle without limit. Deflation, “lowflation” and secular stagnation are therefore unnecessary. They are policy choices’ (Buiter 2014).

The situation we are, in other words, is a choice, and central banks’ intervention to reduce private debt is the most positive and least painful, especially when compared to the options of failed austerity. It is a policy option that should be taken seriously, not just because it has been tested and proven to be effective, but because, as Andricopoulos argues, current policies are leading us into a trap where raising interest rates could trigger a debt crisis: ‘Simulating hitting a debt limit also showed the danger of continuing to rely on expansion of private sector debt. For this reason, keeping interest rates low, or even making them negative, is a dangerous and short-term measure. The answer must be fiscal.’

Should a financial crisis befall Canada or another country, monetary financing of government deficits, combined with bank reforms, provides a way to bring the economy back to balance. It may well be worth running a “high-pressure economy” as mentioned by Federal Reserve Chair Janet Yellen in 2016, and further articulated by Josh Bivens (Bivens 2017). Such an endeavour means restoring demand, and pushing for growth which in turn would boost capital investment and productivity, and could pay for major infrastructure and other projects that could ease countries’ transitions away from reliance on carbon energy.

The 2008 financial crisis is now being followed by a series of political crises, as governments have not only failed to extricate themselves from the mess, but are in denial about its causes. Voters are rejecting centrist elites and turning to fringe political parties and candidates not just in a mix of hope and desperation, but because they can exact political revenge either on scapegoats or the elites who have prospered while they have suffered.

Rather than recognize the real and damaging effects of long-standing economic policies, elites have tended to dismiss such ‘populism’ as irrational. The limit of their self-examination has been to blame themselves for not adequately selling the real benefits of policies like austerity or free trade to people who lost their jobs, homes, pensions and have seen their incomes stall or sink, while politicians of all stripes insisted on cutting their social programs.

It should be self-evident that when governments and central banks enact policies aimed at protecting or increasing the wealth of the wealthiest - while suppressing wages, employment and even economic growth in order to do so - that it will lead to negative economic and political outcomes. Clearly presented alternatives to improve the situation – like running a high-pressure economy – are often rejected or ignored because they do not conform to a failed status quo, even when supported by theory and evidence.

The current global economic situation makes it clear that these policies – to increase the wealth of the wealthiest - have been a spectacular success, but that they are also generating serious political unrest that could trigger economic downturns, and there has been an astonishing environmental cost. While the EU has effectively outlawed Keynesian economics, (and others have tried), in Canada, the U.S., the UK and elsewhere, central banks have the tools to fund not just a New New Deal, but a New Great Compression - it worked before. It may take an intellectual revolution for the better among central bankers to resolve this situation, but intellectual revolutions are always preferable to the alternative.”

Heather Cox Richardson recently wrote this outstanding piece:

“During World War II, when the United States led the defense of democracy against fascism, and after it, when the U.S. stood against communism, members of both major political parties celebrated American liberal democracy. Democratic presidents Franklin Delano Roosevelt and Harry Truman and Republican president Dwight D. Eisenhower made it a point to emphasize the importance of the rule of law and people’s right to choose their government, as well as how much more effectively democracies managed their economies and how much fairer those economies were than those in which authoritarians and their cronies pocketed most of a country’s wealth.”

Under Republican president Theodore Roosevelt, progressives at the turn of the twentieth century would continue this reworking of American liberalism to address the extraordinary concentrations of wealth and power made possible by industrialization. In that era, corrupt industrialists increased their profits by abusing their workers, adulterating milk with formaldehyde and painting candies with lead paint, dumping toxic waste into neighborhoods, and paying legislators to let them do whatever they wished.

Those concerned about the survival of liberal democracy worried that individuals were not actually free when their lives were controlled by the corporations that poisoned their food and water while making it impossible for individuals to get an education or make enough money ever to become independent.

To restore the rights of individuals, progressives of both parties reversed the idea that liberalism required a small government. They insisted that individuals needed a big government to protect them from the excesses and powerful industrialists of the modern world. Under the new governmental system that Theodore Roosevelt pioneered, the government cleaned up the sewage systems and tenements in cities, protected public lands, invested in public health and education, raised taxes, and called for universal health insurance, all to protect the ability of individuals to live freely without being crushed by outside influences.

Reformers sought, as Roosevelt said, to return to “an economic system under which each man shall be guaranteed the opportunity to show the best that there is in him.”

Since the 1970s, central bank policies have been undermining liberal democracy. This zeit needs a new geist, and Central Banks need to be a part of it.

30-

DFL

Thanks Dougald, it's a good topic and I enjoyed your article. A question that came to me as I read it was about individual responsibility. If the central banks and thus the retail bankers lower rates, yes I can afford to take on more debt, but that doesn't make it a right decision. I can choose to stay in my current house and pay off my mortgage sooner.

I'm not here to crap on people, we are all just trying to improve our situations, but I do sometimes wonder that we as individuals have to also make good choices, even when we are being incentivized by bank rates. Better education on financial decision making would help, and so would some leadership from our elected officials to give more messages around not extending oneself financially at every opportunity.

None of that speaks to the reckless bailouts of banks, which I've never really totally understood why there were bailouts and not more loans, or why governments or the public didn't get more equity in exchange for the bailouts.

I listen to the Capitalisnt podcast and their intro always plays the sound bite from Bernie about socialism for the rich and rugged individualism for the poor, and every time I hear it, I think, damn, that's right.

Excellent explainer article! Great reference to Heather Cox Richardson as well, adding relatable context. I'm strongly recommending this read to many.