The Bull Elephant in the Room: The Canadian Economists Slamming Government whose Banks got Multi-Billion Dollar Bailouts

Canada does have a problem with its economy. The biggest problem of all is that the people who are supposed to experts in it have learned nothing in the last 25 years.

Canada does have a problem with its economy. The biggest problem of all is that the people who are supposed to be experts in it have learned nothing in the last 25 years of crises. The seven-ton bull elephant in the room, which is that fifteen years ago, the banks these economists worked for received a massive government bailout. Several of the banks were technically insolvent: including CIBC, Scotiabank and the Bank of Montreal.

The economists who are telling us that we have to be more competitive for foreign private capital, that government plays too large of a role in the economy, work at banks that received $112-billion in public money to keep running. The money didn’t come from government coffers, or from taxpayers, or from running deficits by borrowing from people buying bonds. It was money created by the Bank of Canada, and the U.S. Federal Reserve.

As many have pointed out, if their economic formulas were worth anything, they could have predicted the global financial crisis of 2008-2009: but they didn’t.

One of the features of good ideas is that they make reliable predictions. The fact that the Bank of Canada didn’t see the crisis coming, and that Canada’s banks needed a massive bailout of public money should have been more than a wake-up call: it should have been a call to arms. That bailout really put the lie to the orthodox economic ideas we’ve been living with since 1975, which say that such crises are impossible.

The obvious question for these bank economists should be,

“Why do we have to compete for foreign capital - and why is public money so bad when you got $112-billion of it, to keep you from going broke - when no one else gets the same treatment.”

The answer to that question explains why we have an economic crisis in Canada - in why we have low productivity, a housing bubble.

The biggest problem with Canada’s economy is not inflation. It is crushing personal and household debt, for the very reason that the Bank of Canada, and banks have spent 25 years putting trillions of dollars into increasing the value of real estate and keeping a real estate bubble going, even as wages stagnated, instead of investing in productive investments.

I am not going to say any of this was malicious, or ill-willed. The ideas themselves that people are taught about the economy are used to justify ignoring data. The problem is that the ideas are, as Paul Romer has argued, divorced from reality.

This is exactly what Keynes meant when he wrote “in the field of economic and political philosophy there are not many who are influenced by new theories after they are twenty-five or thirty years of age, so that the ideas which civil servants and politicians and even agitators apply to current events are not likely to be the newest. But, soon or late, it is ideas, not vested interests, which are dangerous for good or evil”

The Canadian Bank Bailout You’ve Never Heard Of

During and after the Global Financial Crisis of 2008-2009, Canada was singled out as a success story because it was one of the few countries in the world that did not have a bank collapse. Paul Krugman wrote about it in the New York Times, Canada’s banks were seen as safe. There were articles about Canada having the world’s “richest middle class.” - the American Dream Moving North. The Daily Show ran a piece on how staid and dull Canada’s banks were compared with the U.S.

In fact, Canadians and the world were misled. In a report for Canadian Centre for Policy Alternatives wrote, David MacDonald wrote that Canada’s banks “received $114 billion in support, a figure equal to 7% of the size of Canada’s economy in 2009… This is equivalent to $3,400 for every man, woman and child in Canada.

Scotiabank, Royal Bank and TD Bank received an estimated $25-26 billion each, CIBC an estimated $21 billion, and BMO received an estimated $17 billion. Most of these happened in early months of 2009, except TD, which peaked in September 2009.

Peak support for Scotiabank hit approximately $25 billion in January 2009, the third highest among Canadian banks.”

Canada Mortgage and Housing Corporation (CMHC, a Government of Canada Crown Corporation) spent $66-billion to take bad mortgages off the banks’ books

In December 2008, Canadian banks borrowed $33 billion from the U.S. Federal Reserve

To put this in perspective: six out of Canada’s ten provinces have a GDP less than $100-billion a year. $112-billion is enough to wipe out the debt of entire provinces and pay for their governments to operate a number of years.

This is also in stark contrast with the Federal Government’s fiscal response that followed. The Federal Conservative Government followed with years of austerity, cutting federal programs (for the military, First Nations, housing) while slashing health, education and social transfers to provincial governments while also cutting taxes. In order to balance their budgets, provinces had to either raise taxes, freeze or cut spending, run deficits, or all of the above.

Where The Money Came From: Thin Air - AKA: “Quantitative Easing”

There is an obvious question here - why is it that governments, “real economy” businesses are expected to tighten their belts and endure years of austerity, or seek loans on the private market, while banks and bondholders can get money that is freshly created by central banks, in the hundreds of billions of trillions of dollars, as has happened in the last 15 years.

That is what “quantitative easing” is - creating money out of thin air. Central banks have the power to create money from scratch. That’s what do, and it’s a critically important power, for a variety of reasons, starting with the fact that it is a guarantee against economic collapse, and is an assurance of some core economic stability, because in an emergency, the Bank of Canada could create money. They cannot run out of “ammunition”. That makes government, and government finances, enormously more stable.

Central banks are not like retail banks.

This is one of the reasons why a government that borrows in its own currency cannot default. When you lend Canadian dollars to the Canadian government, US dollars to the US Government, UK pounds to the UK government, they can always pay it back, because ultimately, they can just create it with a few keystrokes. In the past, it was “fountain pen money” and it was in a ledger.

The Bank of Canada describes quantitative easing here: They buy government bonds (and sometimes corporate bonds), from banks, because they claim this will be good for inflation.

We offer to buy bonds from financial institutions that are willing to sell them to us at the best price. (This is called a reverse auction because we are auctioning to buy—not sell—the bonds.)

To pay for the bonds, we create settlement balances and deposit them into the accounts that financial institutions have at the Bank of Canada.

As the bank says, “QE is not the same as printing cash.” But not all money is cash. Most money is in an account somewhere. The central bank isn’t printing sheets of $1,000 bills, or coins, and putting them into bank accounts.

If this sounds odd, it is. It actually ushered in a new era of economic policy that has yet to be named. The amount of public money printed for this purpose around the world was in the trillions, even before the pandemic, when trillions more dollars were printed.

Because interest rates were so low, central banks kept relying on QE. That became the go-to move. It temporarily solved the problem, and keeps asset and housing bubbles going.

In 2010, the EU faced a currency crisis, in part because their own banks had used AAA-rated mortgage backed-securities as reserves. When those collapsed in value, so did the banks. By 2015, the European Central Bank (ECB) had a quantitative easing program of up to 60-billion Euros per month.

It’s not clear what kind of economic system this is, but one anonymous commentator on the Financial Times of London suggested “financial communism.”

Most money in the economy is just credits and numbers in a database. When you make a purchase with your debit card, no physical money changes hands, and it doesn’t have to. It is all accounting, and it always has been. The value of a coin is the value stamped on it, the value of a bill is what is printed on it, and we enforce that value socially and legally. Cash is just a portable and durable record of credits. The reason we had so many controls around money - and against counterfeiting. That’s what bitcoin is.

This might be strange to wrap your head around, because this is not how most people, including economists, think of money. The value of money is that use it to get other people in your own community and country to do things. Money is extremely useful and powerful, but it also requires a whole bunch of laws, regulation, enforcement and conflict settling to make sure that people actually keep their word.

Our current economic models are “neoclassical” which means they are new version of “classical economic”. In that model of the economy, the government creates money, and people think that if the government spends more money, it creates inflation - as if money is air filling up a balloon.

Neoclassical economics do not include finance (banks) or debt, or, in fact money.

The reason for this is a couple of false assumptions. One is that our economy is really just a barter economy where people are trading goods and services, and money is just a means of facilitating that, so it doesn’t have to count. So money is not modelled, and some economists have even questioned whether it matters (!).

The other is that there is an assumption banks are just a middle-man, and that when you put money in the bank, the bank lends it out your money. This is treated as if the person just owes you money, and that all debt in the world will just cancel out.

This is not how banks actually work, as many economists and central banks have now recognized, and this is the key part to understanding the economy, and what’s wrong with it, and how to fix it.

How Most Money in the Economy is Created

As this article notes, “In contemporary societies, the great majority of money is created by commercial banks rather than the central bank,” which is denominated in the currency of the country where the bank operates. Banks are not lending someone else’s money to you. They are creating money through extending credit, almost like “store credit.”

The UKs’ Central Bank, the Bank of England, described the process in a 2014 paper:

In the modern economy, most money takes the form of bank deposits. But how those bank deposits are created is often misunderstood: the principal way is through commercial banks making loans. Whenever a bank makes a loan, it simultaneously creates a matching deposit in the borrower's bank account, thereby creating new money.

The reality of how money is created today differs from the description found in some economics textbooks:

Rather than banks receiving deposits when households save and then lending them out, bank lending creates deposits.

In normal times, the central bank does not fix the amount of money in circulation, nor is central bank money 'multiplied up' into more loans and deposits.

Although commercial banks create money through lending, they cannot do so freely without limit. Banks are limited in how much they can lend if they are to remain profitable in a competitive banking system. Prudential regulation also acts as a constraint on banks' activities in order to maintain the resilience of the financial system…

Monetary policy acts as the ultimate limit on money creation.

The amount of credit the bank will extend to you - the size of the loan or mortgage - depends on how much you can pay in debt servicing, as well as the interest rate, and other regulations, like regulations on reserves requirements, which set a limit on how much credit banks can extend. These are also detailed in the Bank of England’s paper (the German Central Bank, the Bundesbank, has made the same argument.)

This is the vast amount of money in the economy.

You might well ask, how is it possible for banks to extend credit they don’t have and to create money in this way. There are two big reasons why banks are willing to do this -

1) You have promised to pay them every month for years - much more than they loaned you in the first place.

If you plug $100,000 into this mortgage calculator, 24 years from now when you have paid off the mortgage at 4,79%, you will be paying back $100,000 + another $68,862.

You have signed a promissory note - an IOU to the bank - that you will be making payments every month, and if you don’t the bank can seize what you own.

2) If you don’t, they get to take the house.

Banks are willing to extend credit because it’s secured against an asset. you’re using it to buy an asset, which they will seize and own, and they can then sell, and get real money back.

In Canada, there are millions of mortgages. The interest rate and extra payments aren’t just profit - ideally, the number of defaults will be small. Interest rates and terms are a price on future risk.

And that’s why interest rates are so important to the amount of debt, and who gets it.

When a central bank is supposed to be keeping the economy stable by aiming for a made-up target of 2% inflation, they will “cool off” the economy by raising interest rates (driving people and businesses into bankruptcy) or “stimulate” the economy by lowering interest rates, which is supposed to make money “cheaper.”

However, if a prospective homebuyer wants to buy a house for $300,000 when interest rates were 5%, lowering interest rates to 3% does not mean that they will just get a $300,000 mortgage at 3%. That’s because banks calculate how much you can afford to pay in debt servicing costs per month.

If you’re paying $1000 a month, the bank will extend more credit when interest rates are low, which means they will offer you a bigger loan. People with bad or no credit will qualify for loans they could not get before, and people with great credit can get enormous loans.

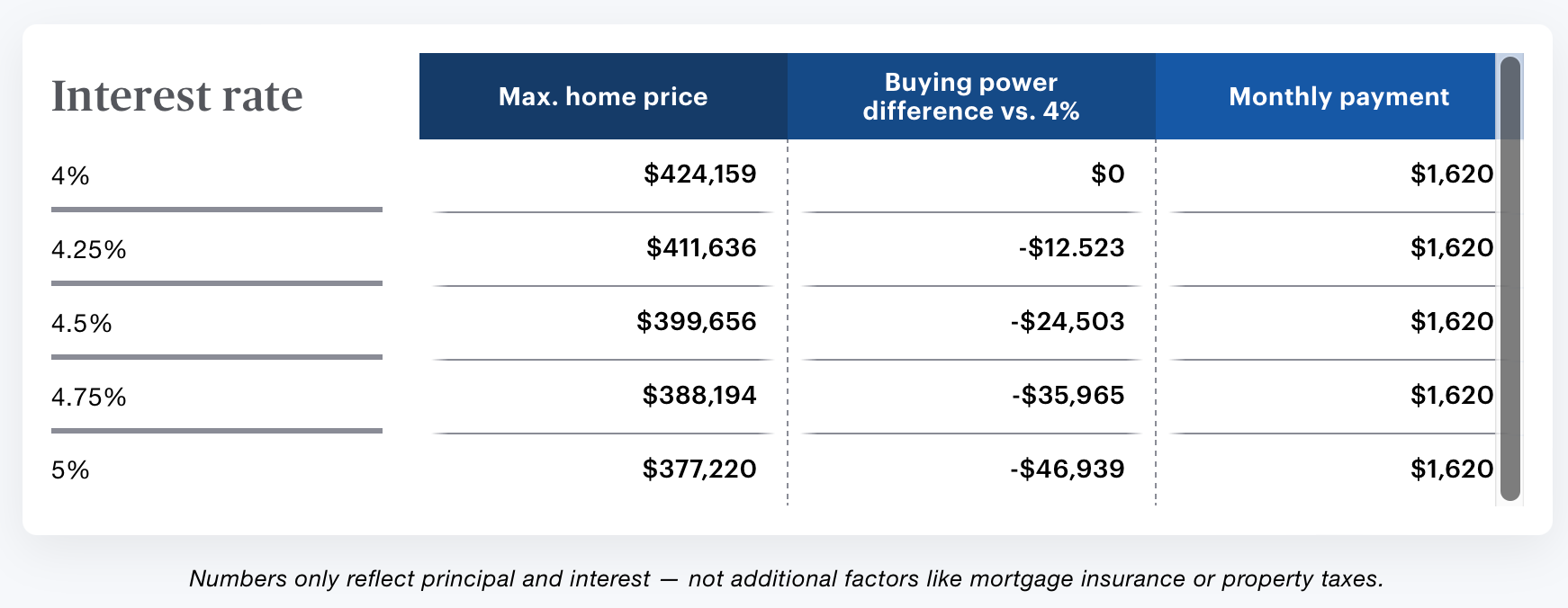

If a borrower can make a $2,000 monthly payment, a 30-year mortgage at 8 percent will finance about a $275,000 home. With mortgage rates of 4 percent, the same payment buys a $550,000 home. The fact that the mortgage is secured against the “asset” doesn’t change that you are borrowing twice the money on the same income.

A slight rate increase might seem minor, but this small increase in your monthly payment can add up over time and affect your buying power.

If you look at a borrower with a monthly income of $4,500 and a debt-to-income ratio of 36% who makes a 20% down payment, even a quarter of a percent increase can mean they’ll be able to afford roughly $12,000 less over the course of a fixed, 30-year mortgage. With a 1% increase, the price of a home they can afford drops by more than $45,000.

The table below shows the difference in buying power for mortgages with rates between 4% and 5%. Even when the monthly payment is the same, the maximum price of a home the borrower can afford goes down significantly when the interest rate increases slightly.

This is the direct link between interest rates and banks’ willingness to extend credit and inject new private money into the economy.

A change in the interest rate of 1%, makes a difference of $46,939 per mortgage. That is a difference in of $50,000 more - plus interest - that the borrower will have to cover. It drives up the price of real estate by $50,000, and it has injected $50,000 in new, privately created money into the economy.

That change by a central bank makes the difference of $50,000 in new debt for a single household. Multiply that across the economy and it adds up to hundreds of billions of dollars.

Because it is credit, and has interest applied to it, it keeps growing. Not all money does that, because not all money is a loan.

If you think this is a shaky foundation, you are right. And it was the foundation of the biggest financial crisis since 1929, the Great Financial Crisis of 2008-2009. It was also the cause of the 1929 crash - because before both of those crashes, interest rates were kept too low, there were massive extensions of credit, which drove up the price of assets - which were non-productive. Houses don’t generate revenue.

So, people were using money they didn’t have to drive up the price of existing assets that don’t generate revenue.

That is one of the reasons that “monetary stimulus” by central banks turning interest rates up and down like a volume knob has massive distorting effects on the economy. It’s a “stimulus” that depends on private individuals and households, some of whom will inevitably not be able to pay.

Two critical points here: not all investments are debt. There is also equity - buying shares in a company that pay dividends only when the company is profitable.

When elected Governments engage in “fiscal stimulus” they can provide transfers, grants, income and revenue supplements, money without debt repayment obligations.

How mortgages and private debt create financial and housing crises

Property booms and financial manias have existed for centuries. Long before 2008, long before 1929, there were property bubbles where people were borrowing to bid up the prices of shares of companies in the Mississippi Scheme or the South Seas Bubble, which are described by Charles MacKay in his evergreen book, “Extraordinary Popular Delusions and the Madness of Crowds.”

Mortgages caused the 2008-2009 global financial crisis, not on their own, but “mortgage-backed securities”, which is investments made out of a bunch of people’s mortgages all bundled together.

If you’re looking for an investment that provides an ongoing source of income, bundling up a bunch of mortgages seems to make sense. If you have many different mortgages, you can get a steady and dependable stream of income. Even if some people default everyone else will keep paying.

So instead of a bank giving you a mortgage and keeping it, they create a mortgage for a homeowner, then sell the mortgage to an investment bank, which would put a whole bunch of mortgages together, and people could then buy shares in that. People can even buy insurance if it turns out people can’t make their mortgage payments.

It seems like a safe bet, but it’s not, from the get-go.

First, the investment is based on the extension of private credit.

Second, the asset being purchased doesn’t generate ongoing revenue.

While people call your home an “investment” it’s not a productive investment that generates ongoing revenue.

If you have a mortgage, you are not making an investment. You are the investment.

You are the one providing a steady stream of interest-based revenue. There is a basic problem here. A personal home is an asset, but it is not a revenue generating investment. It’s not like buying shares in a bakery so a baker can buy new machinery to expand production and generate more revenue to pay you back.

It is an investment where investors and banks are gambling on the ability of the middle and lower classes to pay their mortgages, even as their debt keeps growing and growing, because housing prices are being driven by banks increasing the amount they are willing to lend, even when clients aren’t making more money.

Asset prices are being driven up by banks, who keep extending more and more credit and private debt to more and more people - which they can do, because interest rates are low.

The reason why banks were so willing to make these loans, and that investors are willing to buy these mortgage-backed securities is that the investments were graded Triple A, which means that they are supposed to be as safe as lending money to the U.S. government.

This is simply not a true. It is not reality.

When you lend the U.S. Government U.S. dollars, it is an absolute guarantee that the U.S. Government can pay it back, because the U.S. government has the power to create money. Actual money - not an extension of credit. Cash money or digital bank transfer.

To suggest that an investment made up of a bunch of mortgages is 100% guaranteed is ludicrous, on many levels.

Because the bank will sell the mortgage to be part of an investment fund, they have an incentive to maximize the size of the loan. And because they are graded the same as government debt, banks will buy them and use them for their capital reserves - because they are offering higher interest rates and better returns.

That was one of the reason for bank collapses: bank reserves themselves were made up of investments filled with defaulted mortgages.

During the Global Financial Crisis, there was widespread fraud, forgery and shocking amounts of criminal activity that was never prosecuted, and rarely reported in the broader media. One mortgage company had an “art department” dedicated to making changes on mortgage contracts. It was not just “subprime” mortgages, either - black and hispanic Americans were targeted by lenders who talked them into taking subprime loans, by telling them they didn’t qualify for better rates, when they did.

It is not just in the US where mortgage-backed securities were rated the same as the Government. The same is true in Canada.

A commenter wrote on an earlier post of mine -

Starting in 2001, the CMHC expanded their NHA Mortgage Backed Securities program. The banks create the mortgages, bundle them into securities, the CMHC puts a GUARANTEED stamp on them, and investors buy the securities. Those securities are as secure as Government of Canada bonds. This is now an $11 billion per month operation, with about half a trillion dollars worth of mortgages guaranteed by the full faith and credit of the crown. Investment flows to the guaranteed mortgages instead of to productive businesses.

It would be one thing if these guarantees went into 30 year mortgages for normal families, with the goal of creating stability for citizens, but they’ve gone into all kinds of speculation and chicanery.

The other one is the explicit government guarantee of ALL residential mortgage insurance, public and private. The Protection of Residential Mortgage or Hypothecary Insurance Act was passed in 2011, and guarantees the payment of mortgage insurance benefits for private insurers (for a 10% fee) even if they go bust. The moral hazard is incredible. Why invest in risky commercial ventures when residential mortgages are guaranteed?

The commenter nails the many problems with these practises. It gives private banks a license to print money, both literally and figuratively. They do. The massive increase in the extension of credit made possible by these guarantees, together with ultra-low interest rates and is what has created a housing crisis, a personal and household debt crisis, and problems with productivity.

It has also driven up the price of farmland, as well as the cost of doing business, which makes it harder for small and medium sized businesses, and easier for mega-chains and giants.

Governments have also been reluctant to address this, because a lot of people are making money from it. That’s the problem with financial bubbles - a lot of money is going around and the economy seems to be booming, and no one wants to be the one who shut the party down. In practical terms, it generates revenue for government at all levels - personal, corporate and property taxes, and labour likes it too. It was also good for tax revenues and balancing the budget. It also massively concentrates money and wealth in the hands of a few.

The problem is when it goes wrong, because everyone is drowning in debt, and no one can afford housing anymore, and businesses are shutting down and people are losing their jobs, the money that the banks have been relying on for decades of future income suddenly isn’t there. And if prices across the market are dropping, then the even if the bank seizes the house, they’re not going to get enough money back from the sale to cover the credit that was extended.

That’s what actually happens when a bank collapses. It’s not caused by a bank run. The bank run follows the collapse. People are just trying to get their cash out - but most of the money people had in that bank wasn’t matched by a dollar or pound in a vault.

When these collapses happen in the financial sector, the costs are transmitted to everyone else - the “real economy” of businesses, workers, but also to government. Government deficits go up when the private sector goes down.

The current crisis we are facing is not because of the fiscal or tax choices of elected governments. It is because of central bank policy monetary policy and the expansion of the private money supply by banks extending credit, mostly for speculation in on assets like real estate.

This is why we need to recognize how the economy actually works.

The premise of orthodox/neoclassical economics is that the market, left to itself, will automatically go back to balance and find its own level, and it’s only “outside shocks” to the market that disturb its otherwise perfect workings.

That is not a statement that can be tested, or backed up by evidence. It’s a moral and polical position that if there is anything wrong, it’s the governments fault and the government needs to stop doing whatever they are doing wrong.

Having said all that, this is what the economists said.

The Economists

Stefane Marion of National Trust writes “Attract private investment: Canada’s only way out.” noting that Canada’s productivity has been in bad shape from 2020 to 2023. “With the IMF forecasting unprecedented levels of public debt in all advanced economies, there is no longer any room for large government spending initiatives. This means that the global race among countries to attract private capital will become even more competitive.”

BMO Chief Doug Porter writes that “Finance Minister Freeland has specifically pledged that this year’s fiscal plan will be crafted to set conditions for rates to come down, implying little or no net new stimulus is forthcoming in the April 16 budget.”

Derek Holt of Scotiabank had the spiciest take: “Canada believes in fairy tales” he writes, complaining about the introduction of a new pharmacare program, and also writing this:

“A greater share of GDP is spent on here-today-gone-tomorrow current spending by governments and households than in decades. Tax policy is uncompetitive. Business bashing has become commonplace by people who’ve never spent two seconds working in private industry. Competition policy changes face serious criticisms (eg here). Changes to labour laws have benefited unions while collective bargaining exercises are driving wage growth to the moon despite collapsing productivity. Major sectors of the economy are literally being taken over by government with recent examples being child care, dental care, and now pharmacare. Do we get better quality outcomes in state-run health and education sectors? Tried visiting an ER lately? ‘nough said.”

I’ll say this: that last paragraph is a lot funnier if you imagine it’s being read in the style of stand-up comedian Andrew Dice Clay.

Anyway, between these three commentators, their employers received more than $50-billion in freshly printed public money. To help bail out private banks who had made investments that weren’t paying off.

The Pandemic Blew it Up

The worst part of the way the financial crisis was treated almost as a “false alarm.” Because instead of shifting, Canada kept blowing the asset bubble, in in March of 2020, when the global pandemic struck, governments did exactly what they had done before.

In 2008, the Global Financial Crisis originated in the overnight “paper market” which is a market that is considered extremely safe, and nearly risk free. Companies and institutions may use it to cover payroll. They need to make payroll on Tuesday, they’re getting a payment on Wednesday, so they borrow money for a day.

In September of 2019, there had been massive spikes in interest rates in this market, indicating trouble. Starting in the fall of 2019, The U.S. Federal Reserve intervened with $53-billion of dollars in lending. Because of the chaos of politics in the U.S. and elsewhere few people noticed,

In 2020, central banks once again provided massive “QE” - about $8-trillion.

This has created our housing crisis, it has created our debt crisis, it has created our productivity crisis. It’s not spending on social programs, or health care or taxes that has caused this crisis. It is a private sector crisis created by Bank of Canada’s monetary policy and the way private banks extend credit.

Productivity usually goes up when businesses investments in capital machinery or technology, so employees can accomplish more.

Canada’s banks - have not been investing in productive industry. Instead, we have extended trillions of dollars of credit largely to drive up the price of homes, which don’t generate ongoing revenue.

The Canadian and US and UK housing markets are all about people taking on debt to buy an asset that only costs, and generates no ongoing revenue. Instituional investors are buying up single family housing and renting it to people, with the result that the number of people who own their own homes has plummeted.

What’s more, the high cost of property makes it harder for people in the “real economy” to make a living, because the cost of rent and housing keeps going up, so people need higher wages.

At the level of an entire economy, this creates systemic risk.

In September 2022, Canadian household debt was $2.8 trillion. That is more than 100% of Canada’s GDP. From a bank’s point of view, these mortgages are assets. But from Canadians’ point of view, that is $2.8-trillion in liabilities.

The Bank of Canada has aggressively hiked interest rates, with the result that Canada is seeing people defaulting on their mortgages and businesses going under.

In Ontario, the mortgage delinquency rate was up 135.2 per cent compared with a year earlier, while B.C.'s rate rose by 62.2 per cent. And last November 2023, CMHC warned of “a looming “shock” for borrowers renewing their mortgages as a new analysis shows the pain of higher interest rates is starting to put pressure on some homeowners ‘

The right diagnosis, the right cure

First of all, we need to recognize that the biggest threat to the Canadian economy is not inflation, it is private debt, and the debt has been caused by bad monetary policy and private bank lending that has distorted our economy.

We should heed the analysis of William White, currently a fellow at the C D Howe Institute, White was born in Kenora, Ontario in 1943. He worked “for various central banks for 39 years, most recently serving as chief economist for the central bank for all central bankers, the Bank for International Settlements (BIS)”. His time included working at the Bank of England and the Bank of Canada.

For several years, as economic advisor, White warned Alan Greenspan and other central bankers starting in 2003 - for five years - that there was a financial crisis coming. Greenspan was still surprised when it happened.

The fact that White predicted the crisis that no one saw coming gives him credibility other economists cannot lay claim to. In August 2023, White called for an overhaul of monetary policy in developed countries, because it has:

“Had a variety of unintended and unwelcome consequences that can only worsen; credit “booms and busts”, potential financial instability, fiscal unsustainability, a progressive loss of central bank “independence”, growing inequality of wealth and opportunity and a slower growth rate of potential output. Fourth, as the threat posed by these unintended problems have cumulated over time, “exit” and the “renormalization” of policy has become ever harder to achieve.

To sum up, the current monetary system has trapped us on a path we do not wish to follow because it leads inevitably to ever bigger problems. This is why fundamental reform is needed.”

I’ll get to that in Part Two - coming shortly.

-30-

Excellent analysis. I look forward to part two. I highly agree that the failure to invest in productive activity is a major factor. I also think we should tweak our pension/rrsp rules and ensure more of that money is invested in Canada. The investments represent mobilizing resources, and the factors of production. Economics 101 lists the factors as land, labour, and capital. When the pension funds send our savings abroad, they mobilize foreign factors of production abroad raising their standard of living while neglecting ours. The income that comes back, is for consumption, not for the investment we need to increase and improve our productive capacity.That production is primarily for current consumption like housing, food, clothing, automobiles, computers, medicine, and furniture. However that production is also for investing in more innovative, efficient, capacity for future consumption, investments such as energy, factories, infrastructure, hospitals, schools, transportation, durable goods, and research. Those investments make us more productive and increase our income.