The Deep Economic Explanation For Why We Have Global Far-Right Turmoil: We're in a Massive Financial Bubble, and It's Popping

"Today in the U.S. we are in the fourth superbubble of the last hundred years."

I’ll start by saying that I don’t like writing about things where there is no solution - so the good news I’ll tell you up front - yes, this is a grim sounding article at first, but I want to encourage you that there are practical tools to end the current crisis.

This is from a Nov 7 Vox article on “Why Democrats couldn’t sell a strong economy, in 3 charts” adding “Top-line indicators pointed to cooling inflation and a strong economy. What did Democrats miss?”

“Enduring pessimism about the US economy has puzzled political analysts, given that most major indicators suggest it is strong and that the US has recovered better than other countries from a pandemic-induced slump. Inflation has come down significantly from its peak in June 2022, slowing price hikes for basic goods. The Federal Reserve started cutting interest rates, making borrowing money cheaper. The economy has continued to grow at a solid rate. Unemployment dipped to its lowest level in 54 years in 2023 and stayed within a desirable range.

The reality, as the article points out is that debt is too high, the number of people who have lost their jobs increased by about 680,000 and the claim that

“even if workers received raises that outpaced inflation, that doesn’t help with sticker shock. Research has shown that consumers have an internalized “reference price” — a conception of what constitutes a fair price for a good they routinely purchase. If that imagined price doesn’t match up with reality, consumers feel short-changed.”

I will just say that this assessment of the economy is incredibly important, because it shows exactly why people are blind to the bigger problems.

The reason for the current economic crisis is the one I’ve been writing about in the very first post of this blog: that we are in a massive asset bubble, blown up over decades by central bank policies which exert a level of control and influence over our economy that we usually ignore, downplay, or that theory says does not exist, all evidence to the contrary.

Today in the U.S. we are in the fourth superbubble of the last hundred years.”

I stumbled upon Jeremy Grantham, a billionaire investor who made his fortune as a contrarian - as an investor who detected, and shied away from bubbles, the mania surrounding them, and the crash that follows. It’s routine after financial crashes and disasters for people to say that “no one saw it coming.” Grantham and his company saw several of them. The 1989 bubble in Japan - which is arguably the largest bubble in history - when Japanese real estate was worth 50% of the entire world. One suburb of Tokyo was worth all of California. Another suburb, all of Canada. He also anticipated the 2000 Dot-com crisis, 2008 financial crisis.

His credibility includes being a self-made investment billionaire, based on a simple principle: reversion to the mean.

In 2022, Grantham wrote “Let the Wild Rumpus Begin” where he argued that we are in the one of the largest bubbles in history, and that it’s starting to unravel. And when that happens, it can be extremely economically painful, even as superhigh indicators mask the problems underneath. Even the name “bubble” is a problem, because you have a visual association with it popping and disappearing. Instead, It’s more like the side of a mountain slowly collapsing.

He also explains why we don’t see it: “In a bubble, no one wants to hear the bear case. It is the worst kind of party-pooping. For bubbles, especially superbubbles where we are now, are often the most exhilarating financial experiences of a lifetime.”

He writes, on January 20, 2022:

“This time last year it looked like we might have a standard bubble with resulting standard pain for the economy. But during the year, the bubble advanced to the category of superbubble, one of only three in modern times in U.S. equities, and the potential pain has increased accordingly. Even more dangerously for all of us, the equity bubble, which last year was already accompanied by extreme low interest rates and high bond prices, has now been joined by a bubble in housing and an incipient bubble in commodities.

One of the main reasons I deplore superbubbles – and resent the Fed and other financial authorities for allowing and facilitating them – is the underrecognized damage that bubbles cause as they deflate and mark down our wealth. As bubbles form, they give us a ludicrously overstated view of our real wealth, which encourages us to spend accordingly. Then, as bubbles break, they crush most of those dreams and accelerate the negative economic forces on the way down. To allow bubbles, let alone help them along, is simply bad economic policy.”

If you’re wondering why this wasn’t picked up in the news, we were in our fourth and one of the deadliest waves of covid. Putin and Russia were menacing Ukraine, and a trucker Convoy was making its way to Ottawa.

Grantham continues and explains why, paradoxically superhigh stock prices are not a good economic indicator:

What nobody seems to discuss is that higher-priced assets are simply worse than lower-priced ones. When farms or commercial forests, for example, double in price so that yields fall from 6% to 3% (as they actually have) you feel richer. But your wealth compounds much more slowly at bubble pricing, and your income also falls behind. Some deal! And if you’re young, waiting to buy your first house or your first portfolio, it is too expensive to get even started. You can only envy your parents and feel badly treated, which you have been.

And then there is the terrible increase in inequality that goes with higher prices of assets, which many simply do not own, and “many” applies these days up to the median family or beyond. They have been let down, know it, and increasingly (and understandably) resent it. And it absolutely hurts our economy. Looking back in a decade or two, if bad things have happened to our democracy, the huge surge in income and wealth inequality of the last 50 years (as CEO income moved from about 25x the average worker’s to about 250x) will have carried the largest share of the blame. So, a pox on asset bubbles!

Today in the U.S. we are in the fourth superbubble of the last hundred years. Previous equity superbubbles had a series of distinct features that individually are rare and collectively are unique to these events. In each case, these shared characteristics have already occurred in this cycle.

The penultimate feature of these superbubbles was an acceleration in the rate of price advance to two or three times the average speed of the full bull market. In this cycle, the acceleration occurred in 2020 and ended in February 2021, during which time the NASDAQ rose 58% measured from the end of 2019 (and an astonishing 105% from the Covid-19 low!).

The final feature of the great superbubbles has been a sustained narrowing of the market and unique underperformance of speculative stocks, many of which fall as the blue chip market rises. This occurred in 1929, in 2000, and it is occurring now. A plausible reason for this effect would be that experienced professionals who know that the market is dangerously overpriced yet feel for commercial reasons they must keep dancing prefer at least to dance off the cliff with safer stocks. This is why at the end of the great bubbles it seems as if the confidence termites attack the most speculative and vulnerable first and work their way up, sometimes quite slowly, to the blue chips.

The most important and hardest to define quality of a late-stage bubble is in the touchy-feely characteristic of crazy investor behavior. But in the last two and a half years there can surely be no doubt that we have seen crazy investor behavior in spades – more even than in 2000 – especially in meme stocks and in EV-related stocks, in cryptocurrencies, and in NFTs.

This checklist for a superbubble running through its phases is now complete and the wild rumpus can begin at any time.

What is new this time, and only comparable to Japan in the 1980s, is the extraordinary danger of adding several bubbles together, as we see today with three and a half major asset classes bubbling simultaneously for the first time in history.

When pessimism returns to markets, we face the largest potential markdown of perceived wealth in U.S. history.

In fact, Warren Buffett has largely moved to cash.

Over the last two years, Warren Buffett has been sending Wall Street a message loud and clear – without saying a word. His approach is more cautious than ever and Berkshire Hathaway's eye-popping $325 billion cash stockpile is the outcome of his latest strategy.

Who’s to blame for this? Not politicians, or elected government, or their taxes or their spending. When your whole business is just money - finance - what really affects you is regulation and central banking policy.

He writes:

How Did This Happen: Will the Fed Never Learn?

As of today, the U.S. has seen three great asset bubbles in 25 years, far more than normal. I believe this is far from being a run of bad luck, rather this is a direct outcome of the post-Volcker regime of dovish Fed bosses. It is a good time to ask why on Earth the Fed would not only have allowed these events but should have actually encouraged and facilitated them.

The fact is they did not “get” asset bubbles, nor do they appear to today. This avoidance of the issue seemed to us remarkable as long ago as the late 1990s. Alan Greenspan, who I considered then and now to be dangerously incompetent, famously acted as cheerleader in the formation of the then greatest equity bubble by far in U.S. history in the late 1990s and we all paid the price as it deflated.

Bernanke should have been wiser from the experience of this bubble bursting and the ensuing pain, and he might have moved against the developing housing bubble – potentially more dangerous than an equity bubble as discussed. No such luck! It is pretty clear that Bernanke (and Yellen) were such believers in market efficiency that in their world bubbles could never occur.

This is old territory for me, but I have to admit to enjoying it. Back then, when confronted with a clear 3-sigma event in the U.S. housing market, Bernanke insisted that “the U.S. housing market merely reflects a strong U.S. economy,” and that “the U.S. housing market has never declined.” The information he meant to deliver was unsaid but clear: “and it never will decline because there is no bubble and never can be.” … Whereupon the unprecedented and apparently non-existent housing bubble retreated all the way back to its trend that had existed prior to the bubble, and then quite typically for a bubble, went well below.

Bubbles, Growth, and Inequality

Perhaps the most important longer-term negative of these three bubbles, compressed into 25 years, has been a sustained pressure increasing inequality: to participate in the upside of an asset bubble you need to own some assets and the poorer quarter of the public owns almost nothing. The top 1%, in contrast, own more than one-third of all assets. And we can measure the rapid increase in inequality since 1997, which has left the U.S. as the least equal of all rich countries and, even more shockingly, with the lowest level of economic mobility, even worse than that of the U.K., at whom we used to laugh a few decades back for its social and economic rigidity. This increase in inequality directly subtracts from broad-based consumption because, on the margin, rich people getting richer will spend little to nothing of the increment where the poorest quartile would spend almost all of it.

So, here we are again. This time with world record stimulus from the housing bust days, followed up by ineffably massive stimulus for Covid. (Some of it of course necessary – just how much to be revealed at a later date.) But everything has consequences and the consequences this time may or may not include some intractable inflation. But it has already definitely included the most dangerous breadth of asset overpricing in financial history. At some future date, when pessimism rules again as it does from time to time, asset prices will decline. And if valuations across all of these asset classes return even two-thirds of the way back to historical norms, total wealth losses will be on the order of $35 trillion in the U.S. alone. If this negative wealth and income effect is compounded by inflationary pressures from energy, food, and other shortages, we will have serious economic problems.

At this point, we also now have the AI bubble. Companies are running around building massive data centers so they can find more ways to train AI to replace people’s jobs. It will be the proverbial new fish that gobbles up the old fish before going belly up.

Grantham also made another updated prediction here.

When you get a bubble bursting, a giant domino-chain of private sector bets has gone bad. The government generally doesn’t think it’s a problem, because they’ve got tax revenue coming in as well.

People are very judgmental about people in debt, because they think either that they are always living beyond their means, and that they should be punished for their mistake. The one thing that people should consider is that people can sometimes afford to take a risk that they don’t realize they can’t afford to lose.

There’s also a really important point about money and interest here. When you buy or sell something, or when government spends or taxes, it’s in fixed amounts of money. There’s no interest running on it. But debt grows and must continually eat into and convert money fixed money into debt.

That’s why religions have rules around debt and interest, including Judaism, Christianity and Islam. Debt and interest caused crises, so they created rules around them.

In a system where government, personal and corporations are dealing in money that doesn’t have interest on it - it means that the costs of debt exceed, not just the amount that one lender can repay, but that that interest and fees and all the other hedging can exceed all of the money that exists.

With mortgages, we take big risks that don’t seem risky at the time - because your banker was telling you could afford it. Like taking out a mortgage, when you didn’t realize you’d lose your job, because the price of oil went down, or inflation went up.

What people need to realize is that these crises actually destroy money, and the debt overhang continues to eat into any recovery you are trying to achieve.

That is one of the problems, right now. Commercial real estate has already crashed. We’ve got record homeless and empty office towers.

And again, this really is all at the feet of central banks and what is really a colossal ongoing failure of our current neoclassical / neoliberal economics which deny that a financial crisis can happen, at all. Austrian economics are wrong as well, because they don’t understand that money is not a bunch of solid coins or pieces of gold. It is, and always has been informational, and it’s created, deleted and cancelled out all the time. The money you owe to someone is money. If they tell you you don’t have to pay them back, the money is destroyed.

Money is malleable, but we treat it like it’s graven in stone

What’s odd is that you would think that people who were into both tech and finance would be aware that all information technology exists because of the work in information theory of Claude Shannon, and in Cybernetics of Norbert Weiner. Alan Turing played an important role as well.

All money has always been human symbols. It doesn’t exist outside of human behaviour anymore than languages do. And the thing about information is that it can be used to communicate a message, send a code on how to interpret a message, and also to send a command. That’s the basis of Cybernetics - where we get the term for cyberspace. Cybernetics is the idea of combining action and feedback for control, and both Shannon and Weiner recognized that these rules applied to all types of information. It is not just the fundamental basis of all electrical engineering, AI, feedback, it also applies to natural phenomena like DNA analysis, language, math, and computer languages.

If you really want to understand how money works, it’s actually incredibly useful to think of it as a kind of information. It’s symbolic. It’s basically something you use to get another human being to do something, like sign over their property for it.

Because people are unfamiliar with thinking about money in this way, when you suggest it does work like this, they are unmoored, and experience a kind of intellectual disorientation. People think that if it is information, then it is just “marks on a page,” but that misses the point, twice over.

Humans treat texts incredibly seriously . People have organized societies and religions and communities around common texts. Human beings kill each other over them all the time. They get furious over movies and comics.

Our explanation of money creation and why the economy must run the way it does is not remotely accurate or scientific, and it’s incredibly harmful. It’s a threat to everyone.

This is the problem in the economy right now. That is what is so destabilizing.

The economic and political misery in our countries and in the world right now is because of this massive distortion. It’s why people can’t afford houses. It’s why we’ve got insane inequality. It’s why we’ve got crytpocurrency, the only money that depends on electricity. It’s why young men can’t get good jobs. It’s why people are losing their houses. It’s why unemployment’s going up. It’s why everyone’s screaming at each other and is so mad. It’s why people are taking it out on immigrants, and people who look and think different. Everywhere.

While people keep trying to blame politicians - who loosened regulations and had weak enforcement, especially after the 2008 financial crisis. It is certainly much more what central banks failed to do - despite continual warnings from the Bank of International Settlements. The solution has to be fiscal, not monetary, and these central banks can repair the damage by destroying the excess debt they created. It’s essentially an injection of equity in the individual borrower, replacing debt with equity. This could allow house prices and assets to normalize.

No, Hyperinflation Does Not Work Like That

When the economy crashes, the government does not crash. It might people angry, but the reality is that any government with its own currency, could technically finance all of its budgeted spending and investments through money created by the central bank. It is called a “monetized deficit”. It’s not inflationary, because it’s actually keeping spending level even if revenue drops. This is one of the things government exists to do.

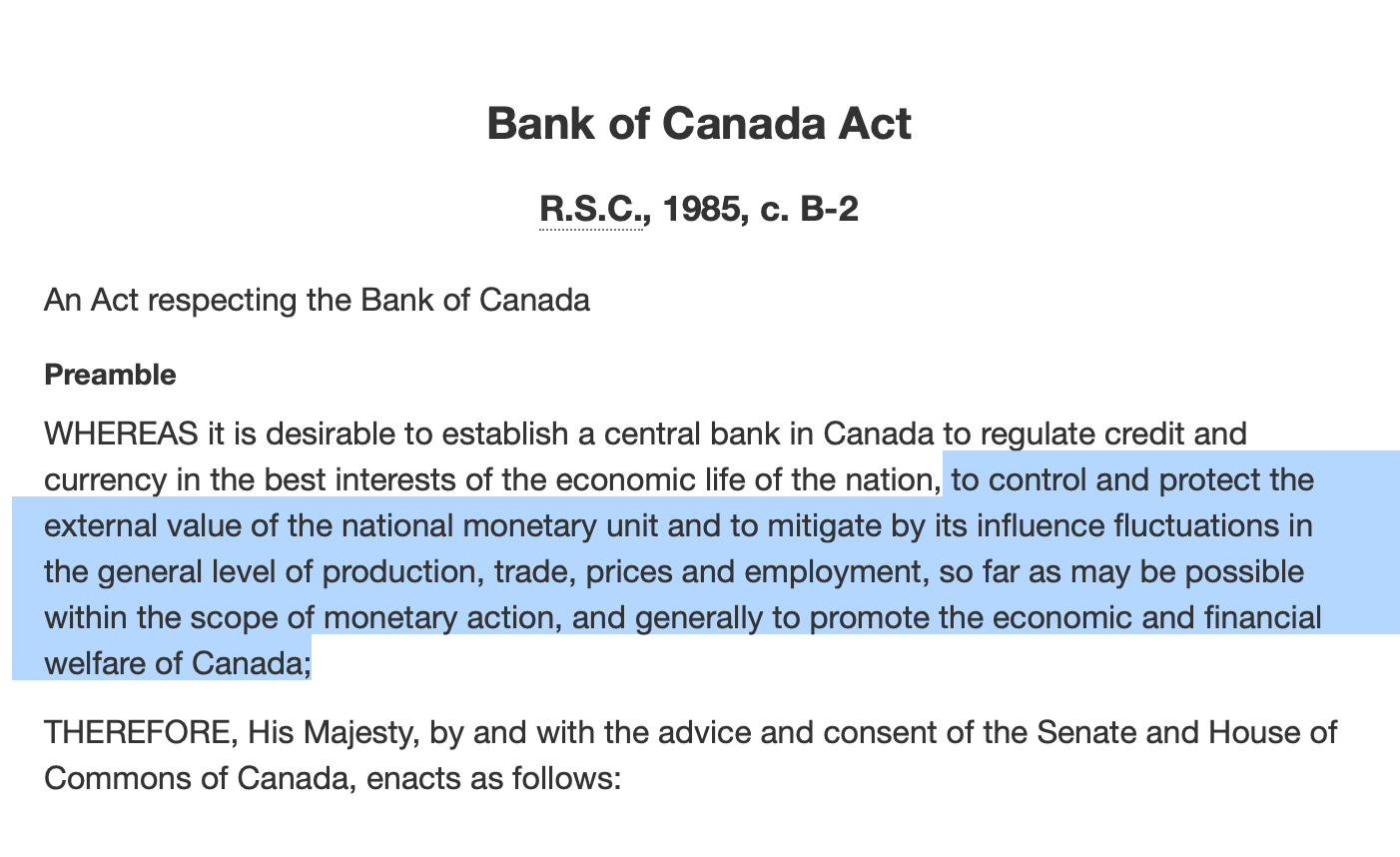

So, the Bank of Canada, or the Federal Reserve and the Bank of England, has the capacity to print money. In Canada, the original mandate of the Bank of Canada Act is basically “anything to fix the economy.”

Governments, and central banks, have the power to create money and use it to employ people, invest, buy shares in corporations. Governments don’t have to fire anyone. All of the spending is someone’s income. They don’t have to privatize anything or so anything to reduce spending. It doesn’t crowd out investment, it crowds it in.

Government and all its laws and regulations are part of the economy too. Government spends money into the economy, then collects money back as taxes. People will say “that’s my money” not government, but if the argument is that government gets all its money from taxpayers, where did the money taxpayers are using come from?

What is required is a New Deal, and that means, working to prevent the worst of a crash, not by continuing to prop up asset prices, but by having the central bank injecting equity in homes by lowering debt. Stability is paramount. You could put the entire economy into a holding pattern by putting a freeze on defaults and the central bank covers costs and overhead - for three months - while government, the private sector, labour, work hammer out a genuine New Deal.

It has to be said, that no matter what people’s political allegiance this is better for the people of each country as well as the global economy. It will be much less costly for all of us, in every possible sense of the word. The division and exploitation we are seeing is because of financial desperation, because we aren’t diagnosing the problem.

Every single nation with its own currency and a central bank that lends in its own currency should know, that they can print money. You do not have to have taxes first. The reality is that we can find ways to pay to put people to work, and start their own businesses in Canada, and in other countries. We can coordinate and be transparent so we’re reindustrializing. There may be challenges with trade, but you cannot run out of money domestically.

That’s part of what all these Austrian and libertarian anarcho-capitalists forget about post-crashes. Capitalism requires capital. So you can hike those tariffs, but unless there’s capital available to local entrepreneurs - ALL of the ones who could run a profitable business - you won’t get domestic investment.

There is no need for an economic crisis to happen, ever. They do. That tells us something is not working, and I will point again to Mr. Grantham - and what central bankers like William White would say.

This truly historic disaster lies at the feet of neoliberal economists and central bankers. While this will be used as an excuse for demanding that the federal reserve be eliminated, that is absolute madness - especially when central banks are the only institution to redress the problem, and they can address it with precision.

We do not have to have a Global Depression. We do not have to have World War III. We can relieve people of the burden of their debt or put people to work, and build new infrastructure with monetized debt. And we can put people to work re-investing in making cities more efficient and rebuilding local industrial capacity, and revitalizing communities and private sector businesses.

That’s why I wrote this - which provides an example of a central bank printing money and using it to finance a 25% one-year personal tax cut, with a minimum payment to make sure every one got a minimum amount. I cite economist William Buiter and his paper “Why Helicopter Money Works - Always.” Milton Friedman also recommended monetized deficits.

As I recently wrote, the details and mechanics of quantitative easing demonstrates the ways in which “Economics 101” is just wrong.

No, it isn’t hyperinflationary - the entire story of German Hyperinflation was also wrong.

Now, the obvious question, I hope, for public officials and central bankers would be what they could do differently to deal with this crisis, from multiple vantage points, as opposed to previous crises.

Which is to say: instead of whistling past the graveyard, admit that this is going on, and then do what needs to be done to prevent the amount of chaos, and negotiate a better deal. Real economy businesses stay open, people keep working, and if people lose their jobs, they get another one.

And for good measure - if a conservative Christian says that forgiving debts is somehow not Christian, please have them read this. I would genuinely like to hear why they would reject it.

I will conclude by saying this.

What is, and has been happening, is that interest has been eating into equity for decades, resulting in ever-greater concentrations of wealth and income. We are living in an uncertain and increasingly unstable world, because the system is designed to be punitive. That belief that the value of money is derived from a fixed number of objects - bitcoin or gold, or silver - means that we force people and the world to conform to these artificial limits, rather than the easiest thing in the world to change - information.

We keep trying to fix money problems without using money. Should we be surprised it doesn’t work?

The result is now universal desperation - desperation on the part of billions in distress, and desperation on the part of billionaires who are running out of ways to meet investors’ targets, desperation on the part of populations who blame each other because they don’t have enough money to buy food or pay for shelter.

Independent Central banks can and have created trillions of dollars at the click of a button, but did so to give lenders more - accelerating the process of converting cash into credit. In order to defuse the damage and massive distortions of this superbubble, that needs to be reversed. The issue is that no one knows how to do that, because their interpretation of the data - “key indicators” - is wrong, and policy responses have been limited to bank bailouts and interest rate manipulation.

It has to be done carefully, and it can be, and most important, central banks can do it acting independently from government, or even coordinating with each other.

In 1896, the progressive populist William Jennings Bryant delivered his famous speech demanding that the U.S. move from a Gold Standard to a “Bimetallic” standard of silver and gold, which he argued would unleash prosperity: “You shall not crucify mankind upon a cross of gold.” What’s needed is a reversal of austerity, which means injections of equity in order to preserve ownership, preserve business, lower costs and more. Money does not reflect the world. It organizes people. We have chaos because people have no money, so people resort to force. It does not have to be this way.

-30-

This is the best thing I have read on money in a while. I have said for years money isn't real, it is a symbol for real wealth which is the total output generated by our collective efforts as a species. Calling it informational makes perfect sense to me.

Central bankers “don’t know” that they have options other than blowing bubbles? This strains credulity.